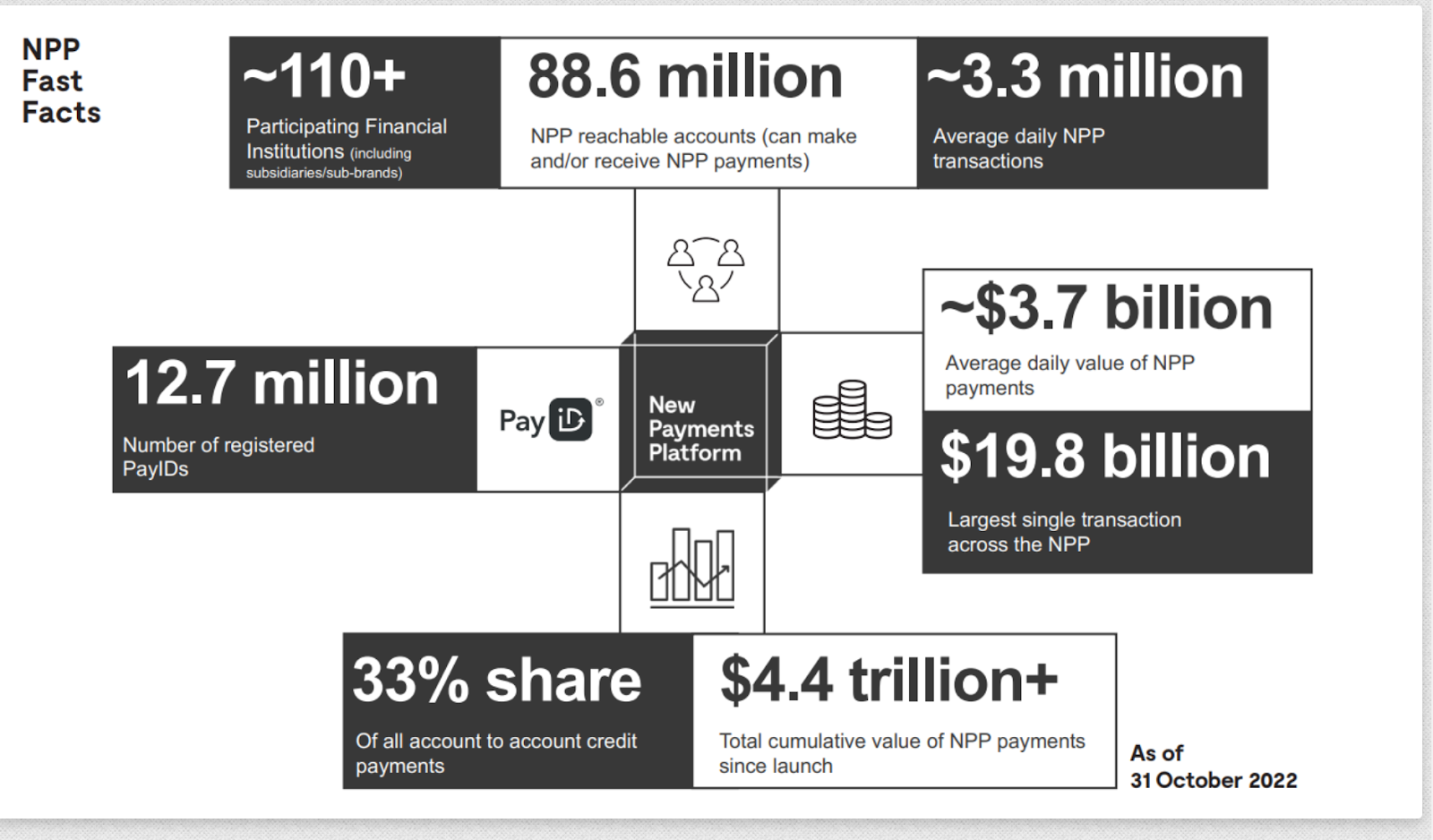

NPP (the New Payments Platform) is an open-access infrastructure in Australia for rapid and safe payments. It was launched in February 2018 and was developed through industry collaboration to allow government, businesses, and households to perform simply addressed transactions, with near real-time availability of funds to the recipient. And this on a round-the-clock basis.

As our research shows, NPP payments messages have the capacity to carry much richer remittance data compared to other available systems in the country. Moreover, this platform’s infrastructure is designed in favor of the “overlay” services’ independent development to provide end-users with up-to-date and practical payment solutions.

We already understand what NPP is, but what about the idea behind it? How was the concept of creating a new payment infrastructure realized, and what was its reason? Let’s have a quick peek.

The Reserve Bank of Australia published the Conclusions of the Strategic Review of Innovation in the Payments System in 2012, setting strategic goals for the country’s payment system. Overall, the review covered such aspects as

- The ability for customers to perform real-time transactions;

- Addressing payments in a comparatively simple manner;

- Sending more complete and detailed remittance information;

- Receiving and sending payments even during non-business hours, etc.

So, NPP was developed as a response to these objectives. It went live in November 2017 and was first used to support payments between a small group of employees from the participating financial institutions and NPP banks.

PayID

One of the leading powers behind NPP’s success is PayID, a well-recognized payment service in Australia.

As the name tells itself, PayID is an ID-based payment method that allows users to make various transactions without going through lengthy and time-eating verification procedures.

With PayID, you just need to sign in to your respective banking app or online platform and use the receiver ID to make an NPP deposit. In general, the ID used on the platform is either the email address or mobile number, so it is quite easy to remember. And if you like gambling, you can easily use it in PayID online casinos.

More importantly, PayID is also famous for its top-class safety policies. Based on our experience, we can say that when using this payment solution for your daily transactions, you can be relaxed as all your data is protected from possible malicious attacks.

But how PayID differs from traditional bank transfers, and what does NPP mean in banking? To have a clearer idea about the main differences, let’s look at this comparative table below.

| PayID | Bank Transfer | |

| Payee ID | Email, phone number, or ABNs | Account Number and BSB |

| Transfer Time | Normally, less than 1 minute | Up to 3 working days |

| Availability | 24/7 | Only Banking Hours |

| Transfer Description | Up to 280 characters | 18 characters |

| Full Payee Name | Confirmed before the approval | Not available |

| Switching Banks | Create a new PayID or keep the existing one | New account number plus new BSB |

Osko

Launched in 2018, Osko is a payment solution from BPAY that operates as an overlay service on NPP. It’s designed to facilitate and simplify real-time funds transfers between businesses and individuals.

As BPAY claims on the Osko website, this service enables users to transfer funds from one bank account to another via PayID or a BSB and account number in less than a minute.

One notable feature of Osko is that transactions can be made with longer descriptions. The characters can include emojis, numbers, letters, and symbols. This can be really helpful for people who receive a large number of payments on a regular basis and need in-depth invoice information or reference.

PayTo

PayTo, previously known as the Mandated Payments Service, is an up-to-date digital payment method providing a fast, simple, and risk-free way to make transfers. It gives users more control and visibility over their transactions and allows businesses and merchants to initiate payments in real-time from their customers’ bank accounts.

In simple words, PayTo is a virtual alternative to direct debits that enables you to make payment agreements with companies or individuals who offer PayTo. This can make managing your memberships, bills, and other expenses several times easier.

The way PayTo works is also straightforward. A business or person needs to set up a Payment Agreement with you. Once done, it’s your turn to authorize when and how much you will pay for certain services or goods. It can be an ad-hoc, one-off, or recurring payment.

After you have authorized, the other party can debit your account based on the terms that you have agreed.

Supporting International Payments

For processing the final domestic leg of an entering international transfer on the NPP, the platform has designed a special business service. It was developed with the goal to support CTF/AML compliance requirements of all sides taking part in these payments processing. As such, this service can be used not only by Australian banks but also by international payment services.

Precisely, the abundance of data of the payment message made on NPP creates all the conditions for the inclusion of extra data when processing a global payment.

Thus, the ability to include additional information and flag the NPP transfer as a cross-border payment means that the NPP will support faster international transactions.